The latest market figures indicate a modest but notable return to growth across the European electronic components sector.

While this development provides a welcome signal of recovery, it must be viewed against the backdrop of persistent geopolitical tensions and the continent’s continued reliance on external sources for key technologies and materials. This dependency exposes Europe to volatility and underscores the fragility of global supply chains, which remain susceptible to political, economic, and logistical disruptions.

Hermann Reiter, Chairman DMASS Europe said: “After a prolonged period of stagnation, the European electronic components market is showing the first signs of renewed momentum – yet structural dependencies and supply chain vulnerabilities remain a critical concern beside the fragmenting customer markets.”

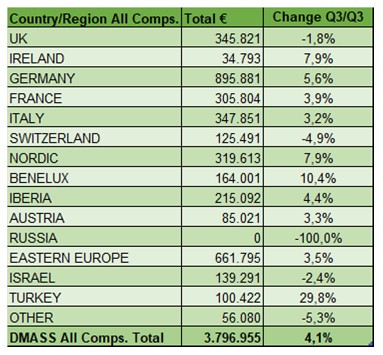

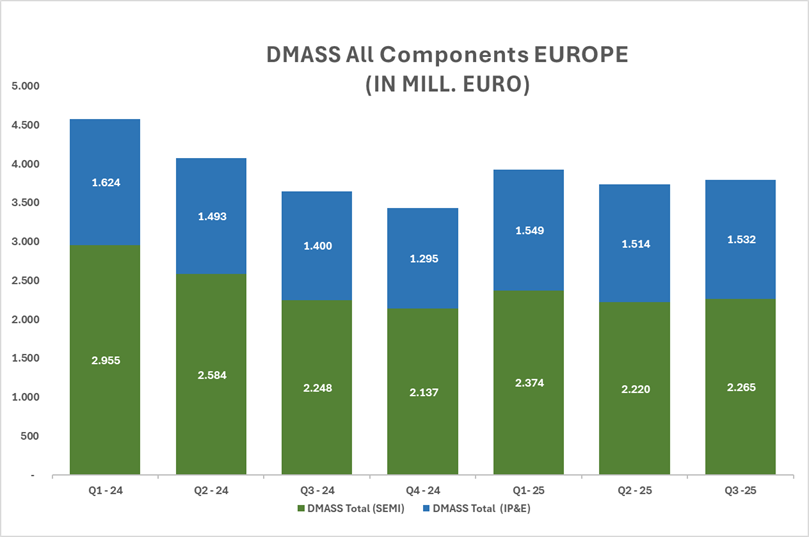

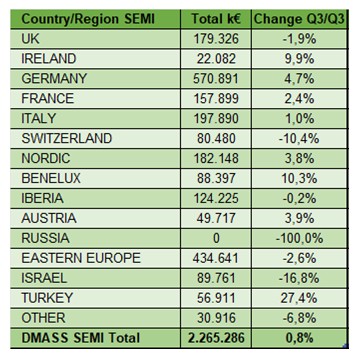

European semiconductor distribution saw a modest uptick, reaching €2.26 billion (+0.8%) in sales. However, several regions remained in negative territory compared to the same quarter last year – including Eastern Europe (-2.6%), Iberia (-0.2%), Israel (-16.8%), the UK (-1.9%), and Switzerland (-10.4%). The strongest growth came from Turkey (+27.4%) and Benelux (+10.3%), signalling dynamic momentum.

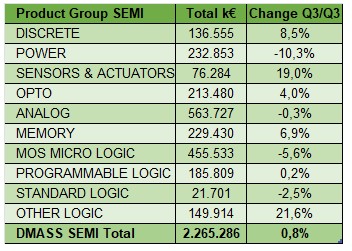

On the product side, Power (-10.3%) and MOS Micro Logic (-5.6%) recorded the weakest sales. In contrast, Other Logic (+21.6%), Sensors & Actuators (+19.0%), and Memory (+6.9%) outperformed the market average of +0.7%, showing notable growth.

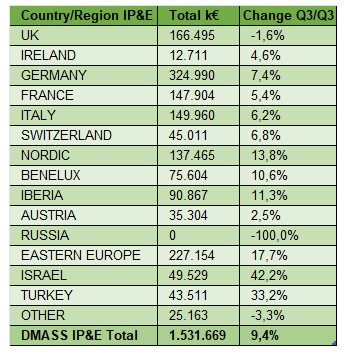

In IP&E, the positive momentum from Q2 accelerated into a notable year-on-year increase of +9.4%, reaching €1.53 billion. Israel stood out with a remarkable +42.2% growth – defying its national trend in semiconductors – while Turkey also posted a strong +33.2%. On the other end of the spectrum, the UK (-1.6%), Austria (+2.5%), and Ireland (+4.6%) remained below average. Germany, Italy, and France further weighed down the overall performance.

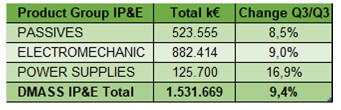

Product wise, Passives (+8.5%) and Electromechanical components (+8.9%) made a solid comeback, while Power Supplies (+16.9%) delivered a particularly strong performance.

The steepest decline was seen in Batteries and Accumulators (-9.0%), whereas Ceramic Capacitors grew by +13.2%, and AC/DC Converters posted a healthy +28.9% increase.

Reiter concluded by saying: “Accelerate relentlessly fast: the European economy in 2025 remains challenged but resilient. In Q3’s crucible of chaos and opportunity resilient amid raw material roulette, turbocharged by AI, aero-military booms, and eyeing government gold rushes that gleam brighter in promise than delivery. These challenges are real – but so is our resolve.

“Europe must not only adapt but actively shape the global dynamics of a rapidly evolving electronics landscape. Let’s seize the reins and redefine the global game.

“Europe – no waiting, full throttle forward.”