Counterpoint Research says the semiconductor industry has formally entered the ‘Foundry 2.0’ era, a phase defined by the deep integration of manufacturing, assembly, and testing, with profitably driven by the global AI boom.

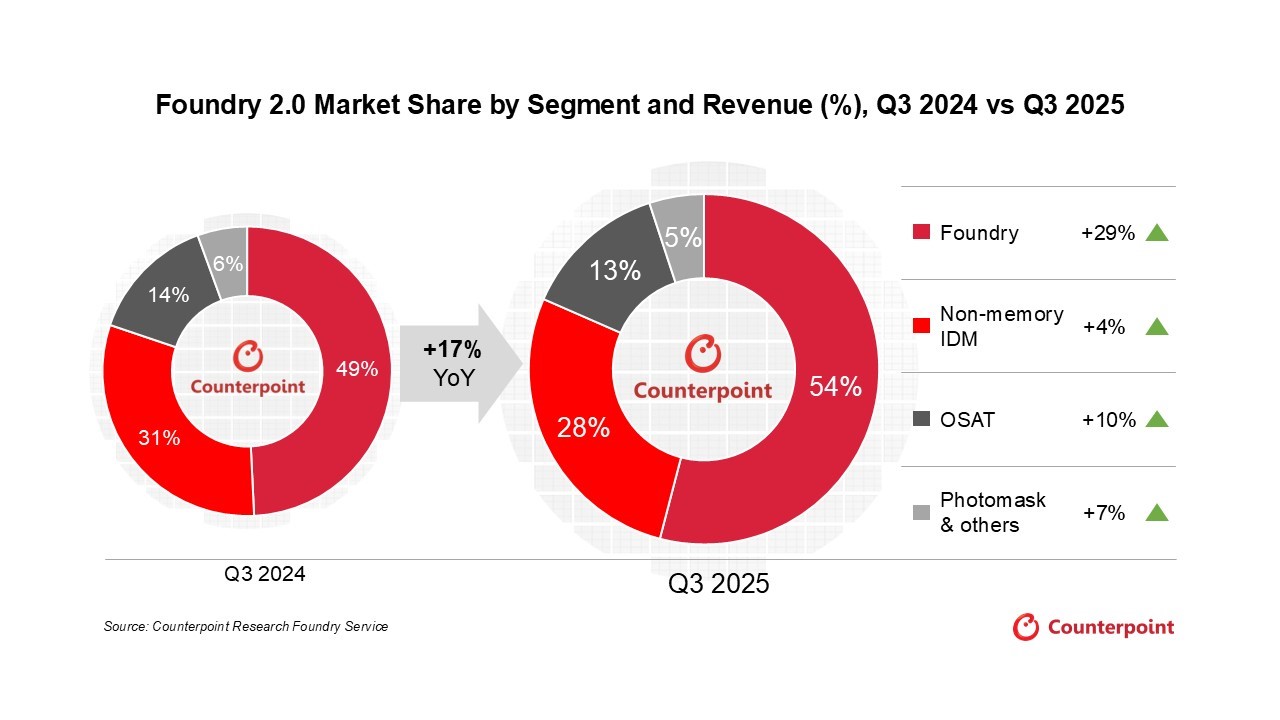

According to Counterpoint Research’s latest Foundry Revenue, Yield and Utilisation Rate by Node Tracker, the global Foundry 2.0 market’s revenue rose 17% YoY in Q3 2025 to reach $84.8 billion.

The double-digit growth was primarily fuelled by sustained demand for AI GPUs across both front-end manufacturing and back-end advanced packaging, with pure-play foundries like TSMC leading the charge and Chinese vendors benefiting from domestic subsidy programmes.

The traditional ‘Foundry 1.0’ definition – focused solely on chip manufacturing – is no longer sufficient to capture current sector dynamics, says Counterpoint.

The company’s ‘Foundy 2.0′ definition expands the scope to include pure-play foundries, non-memory Integrated Device Manufacturers (IDMs), Outsourced Semiconductor Assembly and Test (OSAT) companies, and photomask suppliers.

“Companies are moving from being part of a manufacturing line to acting as technology integration platforms,” said Neil Shah, Research VP at Counterpoint. “This shift ensures tighter vertical alignment, faster innovation, and deeper value creation essential for system-level optimisation in the AI era.”

Among pure foundry players, TSMC continued to outperform the foundry market. Its 41% YoY revenue growth was largely due to the ramp-up on flagship smartphone solutions for Apple in 3nm and full 4/5nm utilisation for AI Accelerator customers such as NVIDIA, AMD, and Broadcom. At the same time, tight utilisation of 4/5nm nodes has become a limiting factor for TSMC’s Q4 revenue growth. However, TSMC’s strong and reliable advanced packaging capabilities will continue to drive its revenue growth in 2026.

The non-TSMC players collectively registered a moderate growth of 6% YoY in Q3 2025 (vs 11% YoY in Q2 2025). However, China-based foundries outperformed with 12% YoY growth, supported by local policies and despite a general diminishing of orders from tariff pull-ins.

Non-memory IDMs returned to growth (+4% YoY), signalling the end of the inventory digestion cycle. Texas Instruments led with 14% growth, while STMicroelectronics showed signs of alleviating decline.

The OSAT segment remained hot and witnessed a 10% YoY revenue growth in Q3 2025 (vs 5% YoY in Q3 2024). ASE/SPIL was the biggest contributor to the growth in the quarter, thanks to the FOCoS (Fan-Out Chip on Substrate) solution benefiting from spillover orders from TSMC to meet the AI GPU and AI ASIC demand. We believe there will be a substantial capacity ramp-up in 2026 (+100% YoY) and thus AI GPU and AI ASIC will be the major growth drivers for OSAT vendors in 2025-2026.

On the outlook for the remainder of the year, Senior Analyst Jake Lai said: “As the primary revenue growth drivers reach utilisation limits (fully loaded 4/5nm capacity) and CoWoS capacity faces constraints, TSMC, which is set to drive overall foundry market growth in 2025, is unlikely to deliver another significant QoQ revenue growth in Q4. As a result, we expect full-year revenue growth to come in at around 15% for overall foundry 2.0 market. The pure-play foundry market is projected to grow 26% YoY and will be the key contributor to overall market expansion, underpinned by sustained shipments of AI GPUs and AI ASICs over the next few quarters.”

On advanced packaging trends, Senior Analyst William Li commented: “NVIDIA and Broadcom are playing the most important roles in the AI GPU and AI ASIC market. Their demand fluctuations cause substantial impacts on the overall CoWoS demand. In 2026, we expect TSMC to mainly focus on NVIDIA’s AI GPU production, namely Blackwell and Rubin platforms. This creates a strategic opening for OSATs. Broadcom and others must seek partnerships outside of TSMC to secure CoWoS-S capacity. This spillover demand will be a key driver for ASE/SPIL’s expansion momentum beyond 2025, particularly for AMD’s Venice and NVIDIA’s Vera platforms in 2026.”