Yole Group announces the release of its annual market and technology report, Status of the Compound Semiconductor Industry 2026 – Focus on Substrates and Epiwafers, highlighting sustained structural growth through 2031.

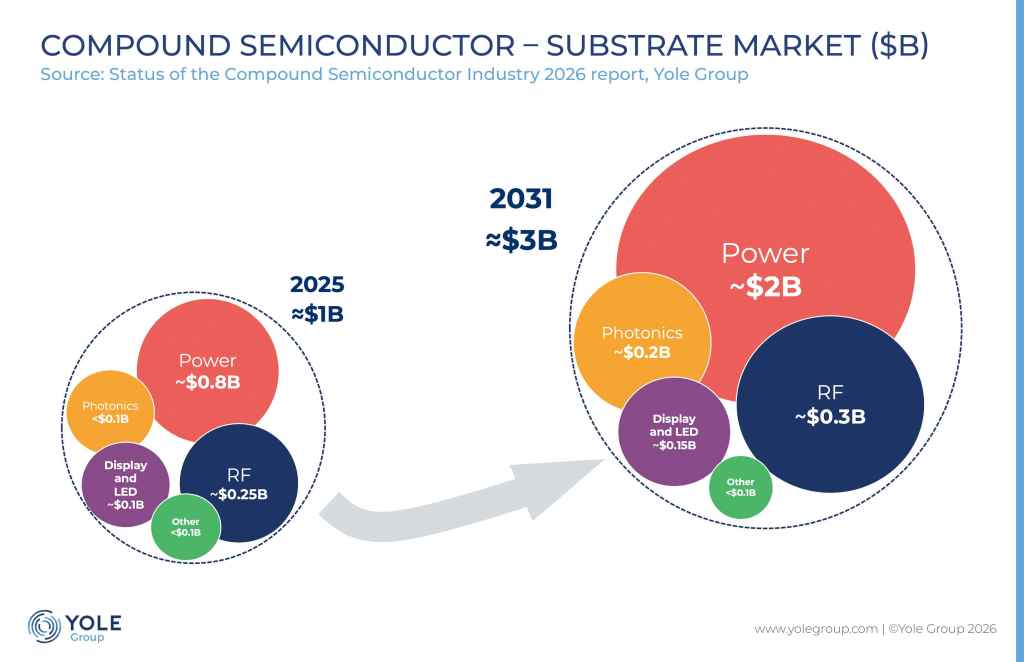

Despite short-term pricing pressure in certain segments, electrification, AI infrastructure expansion, and next-generation connectivity are reinforcing long-term demand for compound semiconductor materials, including SiC, GaN, GaAs, and InP. The combined compound semiconductor substrate and open epiwafer markets are projected to grow to more than $5 billion in 2031, reflecting a ~14% CAGR between 2025 and 2031.

“Power SiC continues to anchor market expansion. What is particularly notable is the diversification of growth. In this new edition, we see this industry becoming structurally stronger and more balanced,” said Ahmad Abbas PhD, Technology & Market Analyst, Compound Semiconductor at Yole Group.

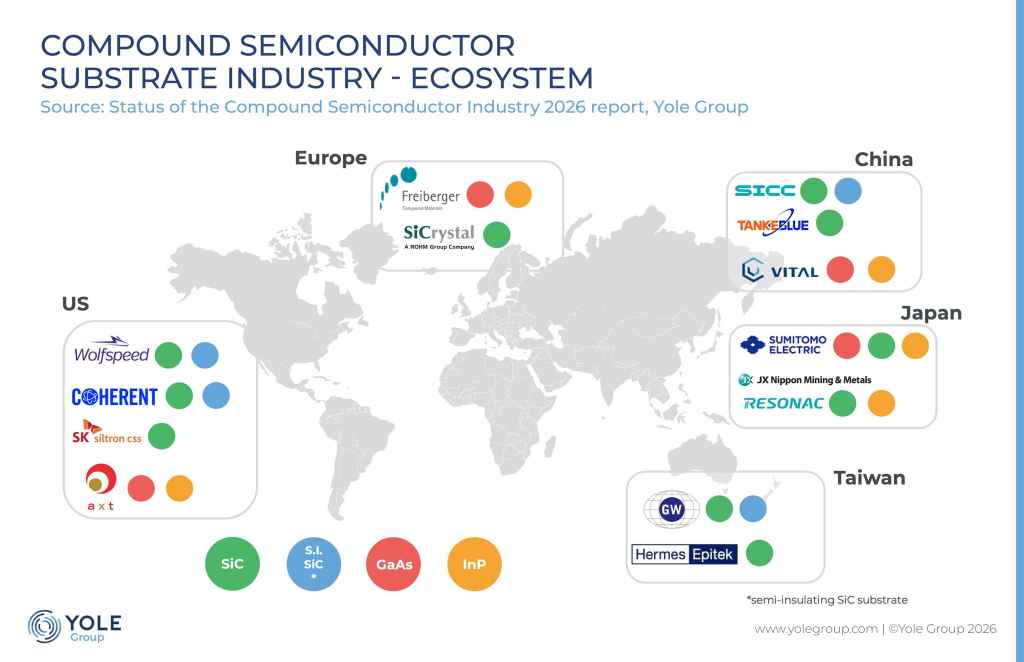

Yole Group’s Status of the Compound Semiconductor Industry 2026 – Focus on Substrates and Epiwafers report provides a comprehensive assessment of substrate and open epiwafer markets across power, RF, photonics, and display applications, with forecasts through 2031. It analyses material evolution, wafer-size transitions, competitive positioning, and ecosystem dynamics. Yole Group’s study also examines capacity expansion, vertical integration strategies, and regional supply chain developments shaping the next phase of industry growth.

“In this edition, we would also like to highlight the key role of AI. Without doubt, AI is reshaping the overall compound semiconductor supply chain: from SiC enabling efficient power delivery in data centres to InP supporting high-speed optical interconnects, compound materials are becoming essential to scalable AI infrastructure,” said Poshun Chiu, Principal Analyst, Compound Semiconductor at Yole Group.

The adoption of compound semiconductors is accelerating thanks to their clear performance advantages. At Yole Group, analysts are closely monitoring this shift across diverse market segments:

Power electronics remains the dominant growth engine. N-type SiC substrates alone are expected to surpass $2 billion by 2031, supported by electric vehicle adoption, 800V architectures, onboard chargers, renewable energy systems, and industrial electrification. The transition from 6-inch to 8-inch wafers is accelerating cost reduction and scaling efforts, reinforcing SiC’s long-term competitiveness despite recent pricing pressure linked to overcapacity and the normalisation of automotive demand.

Power GaN continues expanding beyond consumer fast charging into automotive and data centre applications, strengthening its strategic position as a complementary power technology.

In RF markets, GaAs maintains leadership in handset front-end modules, while GaN progresses in telecom infrastructure and defence applications, with long-term prospects in 6G deployment.

Photonics represents the most dynamic segment. InP substrates are forecast to grow at more than 18% CAGR through 2031, driven by AI data centres, high-speed optical transceivers, and co-packaged optics architectures. The transition to 6-inch InP platforms supports both performance scaling and manufacturing efficiency. Meanwhile, LED remains mature, and MicroLED adoption progresses gradually, beginning with high-end wearable and display applications.