For much of the past decade, semiconductor procurement strategies have been optimised for efficiency. Just-in-Time inventory models, lean buffers, and tightly synchronised supply chains reduced working capital and improved responsiveness. However, the experience of 2024 and 2025 has exposed the limitations of such an approach. No longer an occasional disruption, lead time volatility has become a recurring feature of a structurally changing market. The challenge for buyers is not simply reacting to longer lead times but learning how to interpret them.

Rather than treating lead time extensions as a blanket signal of shortage, they should be understood as indicators of risk – sometimes systemic, sometimes category-specific, and sometimes isolated to individual manufacturers. Read correctly, lead time data like that present in Avnet Silica’s quarterly Trendliner reports becomes a planning tool rather than a source of uncertainty.

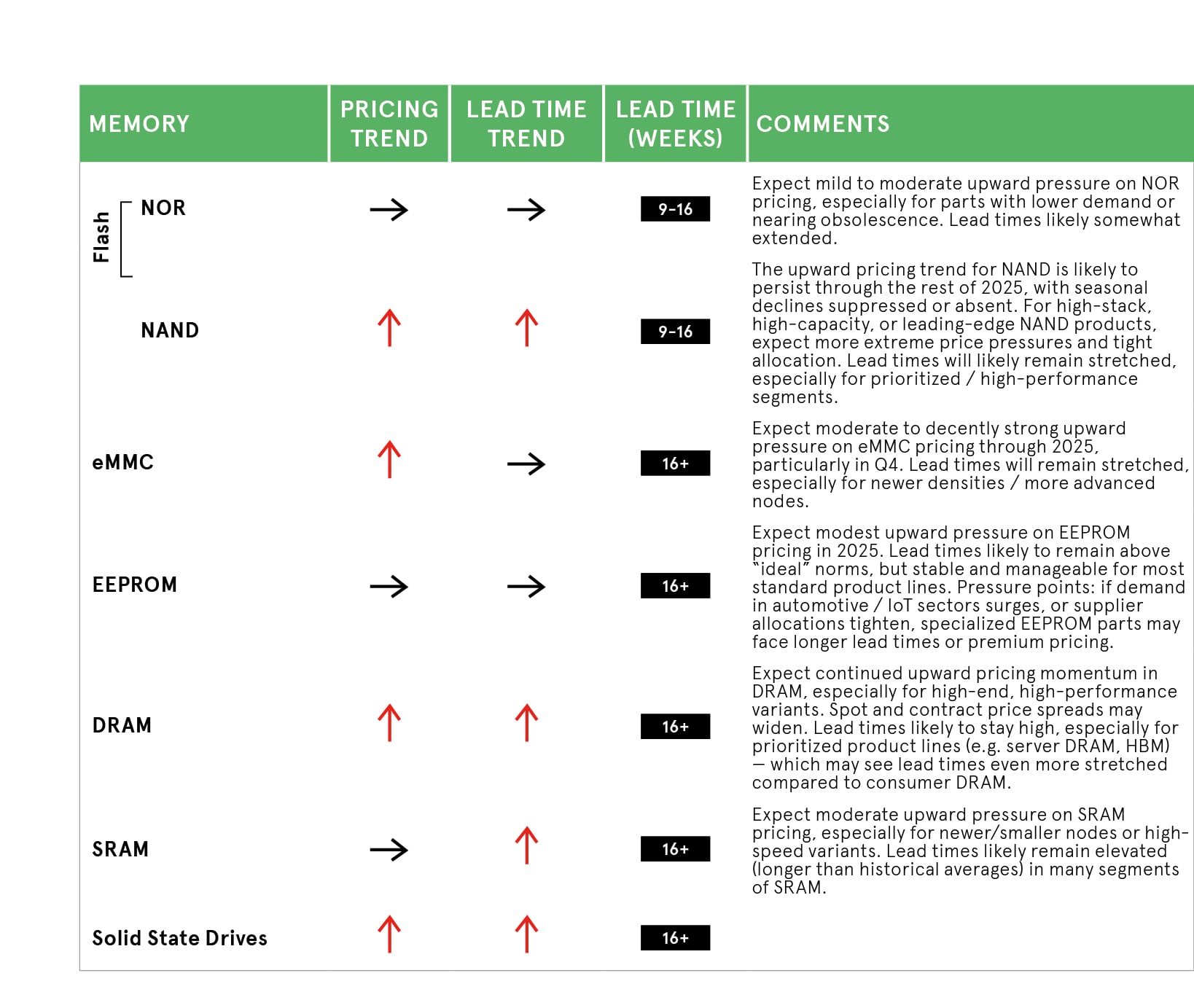

Systemic signals: what NAND volatility reveals

The behaviour of NAND flash over the past year provides a clear example of systemic stress as opposed to transient disruption. Demand for these products recovered through 2024 and accelerated in 2025, driven by data centre investment, AI infrastructure, and storage-intensive applications. The consequent extension of lead times for NAND devices was not the result of panic buying or sudden supply failure, but rather an indication of a market where capacity had been deliberately constrained during the previous downturn.

NAND manufacturing is capital intensive, geographically concentrated, and highly sensitive to utilisation rates. When demand rebounds, capacity cannot be restored overnight. In this context, longer lead times are a structural signal, reflecting the physical restrictions and economics of the supply base, not temporary inefficiency.

For buyers, the lesson is that diversification and buffer inventory are not defensive reactions but strategic assets. Where capacity is concentrated and elasticity is low, reliance on minimal inventory magnifies exposure. Lead time expansion in NAND has therefore been a predictable outcome of broader market dynamics, reinforcing the need for procurement strategies that recognise structural risk early.

Strategic stocking in practice: the SRAM case

If NAND illustrates systemic pressure, SRAM demonstrates how early trend recognition can materially reduce impact. During the first half of 2025, SRAM lead times began to lengthen gradually, moving from a historically stable range of two to eight weeks toward double-digit territory. By Q4, many lines had extended to 16 weeks or more (Figure 1).

What is notable is not the expansion itself, but its visibility. The Trendliner data showed the inflexion well before lead times became operationally disruptive. Buyers tracking Q2 and early Q3 signals had a potential opportunity to adjust stocking strategies, secure allocation, or qualify alternates before the market tightened further.

This is the core shift in modern supply-chain resilience: moving from reactive mitigation to anticipatory planning. Strategic stocking, informed by trend indicators rather than headlines, allows organisations to absorb volatility without resorting to emergency procurement or excessive premiums. In this context, increasing inventories is a valid optimisation strategy, rather than an indicator of inefficiency.

Separating market stress from manufacturer risk

A critical skill in this environment is distinguishing between broad market pressure and manufacturer-specific constraints. Not all lead time extensions carry the same implications. Some reflect genuine capacity strain across an entire category; others point to supplier concentration, portfolio gaps, or operational disruption at individual vendors.

The 2024-2025 data shows increasing divergence between suppliers within the same component families. In some cases, comparable parts exhibited sharply different availability profiles, indicating that risk was not evenly distributed. Buyers who treat all lead time changes as market-wide signals risk missing these nuances.

This is where comparative analysis becomes essential. Understanding how lead times move relative to peers allows procurement teams to identify when diversification, redesign, or supplier substitution can meaningfully reduce exposure. Seen this way, lead time volatility becomes a diagnostic signal rather than a simple warning.

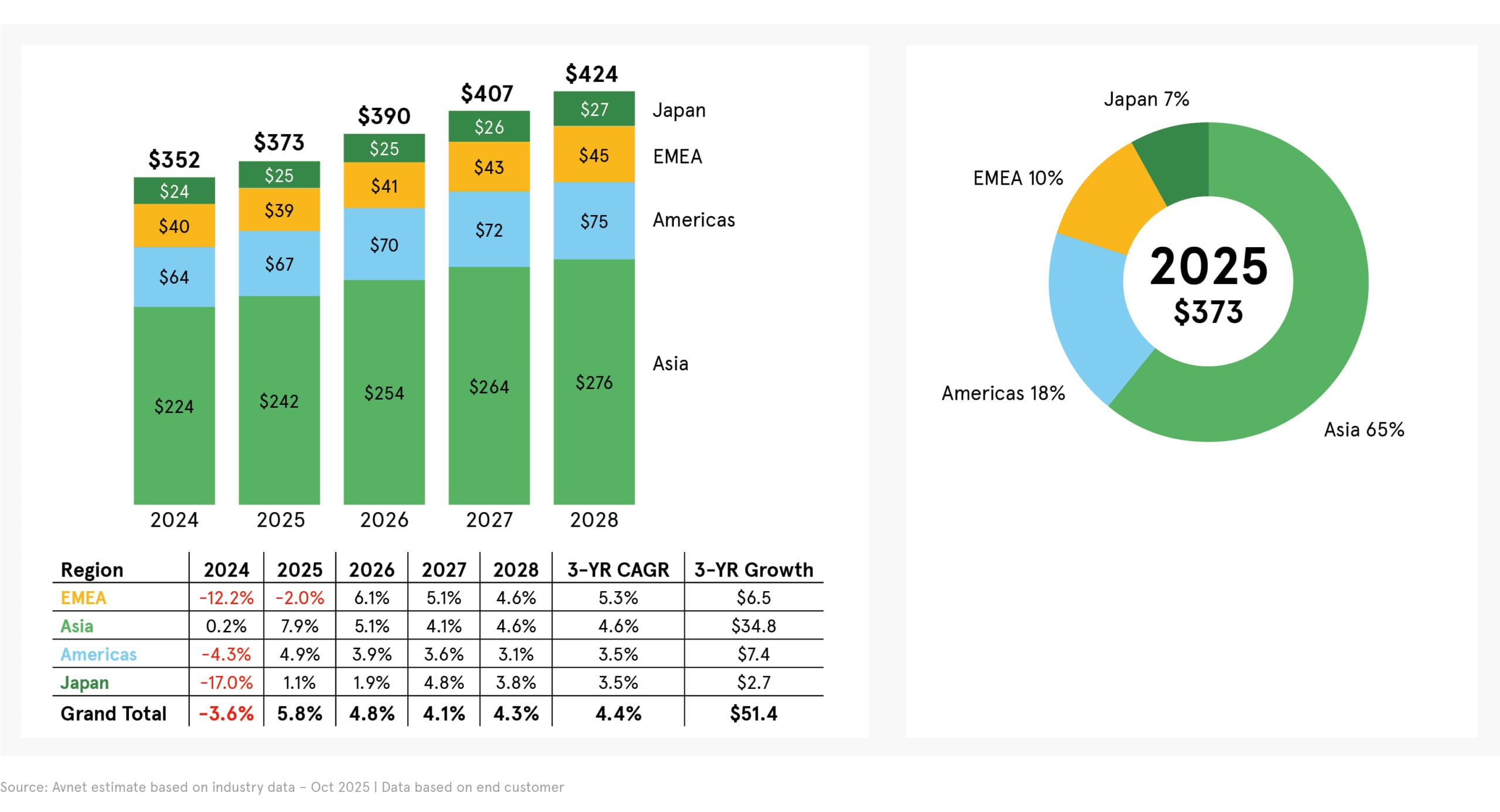

A constructive outlook: capacity investment as the release valve

While short-term volatility has increased, the medium-term outlook is notably more positive (Figure 2). Investment data points to a renewed expansion cycle, with semiconductor capital spending projected to rise by approximately 6.1% in 2026. Importantly, this investment is not limited to incremental capacity increases but is increasingly directed toward localised and regional manufacturing.

Figure 2. While short-term volatility has increased, the medium-term outlook is notably more positive

These developments suggest that current lead time pressures are not permanent constraints but transitional ones. New facilities, once online, will improve supply elasticity and reduce geographic concentration risk. However, the lag between investment commitment and operational output means that 2025 remains a bridge period.

In this context, inventory investment today serves a strategic purpose: it bridges the gap between constrained supply and future resilience. Rather than signalling pessimism, disciplined stocking reflects confidence that today’s volatility will be resolved by tomorrow’s capacity.

Summary: from uncertainty to advantage

The evolution of Just-in-Time strategies does not mean abandoning efficiency; it means redefining it. Lead times are no longer just delivery metrics – they are signals of where risk resides and where planning must adapt. Buyers who learn to interpret these signals, differentiate their causes, and early action can turn volatility into a competitive advantage.

Seen this way, the data from 2024 and 2025 makes one point clear for 2026 and beyond: resilience is not built by predicting the next disruption, but by recognising structural patterns as they emerge. Strategies such as building close distributor relationships and Avnet Silica’s Trendliner support this shift in mindset, enabling buyers to move from reacting to shortages to managing risk with intent. Ultimately, it can be the difference between being positioned not just to endure market cycles, but to navigate them with confidence.

About the author:

Thomas Foj, Vice President Supplier Management, Solutions & Digitalisation EMEA, Avnet Silica

This article originally appeared in the Jan/Feb 26 issue of Procurement Pro.