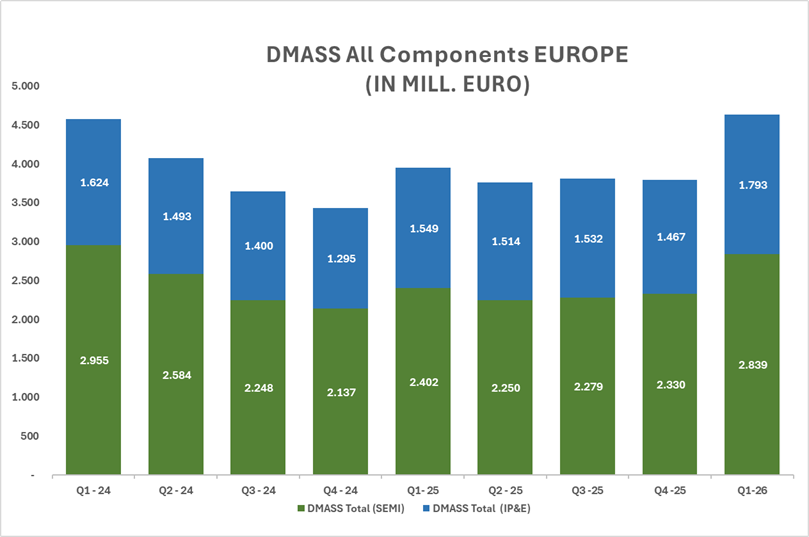

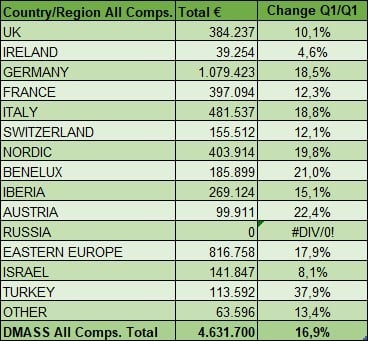

The European electronic components market returned to solid growth in Q1, reaching €4.63 billion (+16.9%), with broad but uneven momentum across the region.

Core industrial economies such as Germany (+18.5%), Italy (+18.8%), the Nordics (+19.8%), Austria (+22.4%), and Benelux (+21.0%) delivered strong double-digit gains, while Ireland (+4.6%) and parts of Southern Europe expanded more cautiously. The exceptional growth in Turkey (+37.9%) reflects shifting regional trade patterns and the country’s increasing role as a logistical and commercial interface in a complex geopolitical environment. Russia remains at zero, as sanctions continue to halt all electronic component flows.

Product wise, the upswing is driven primarily by industrial and automation demand, while automotive related segments show a more muted recovery.

Overall, Europe is growing steadily, though the pattern remains heterogeneous and shaped by structural dependencies, energy market volatility, and an AI cycle that is far more dynamic in the US and China than within Europe itself.

“The positive trajectory from late last year continues, supported by firm pricing, but concerns over availability and pressure on supply chains are increasingly visible,” says Hermann Reiter, Chairman DMASS Europe. “Global instability, including regional conflicts and shifting energy markets, adds uncertainty to industrial momentum without overshadowing the underlying growth potential. What we see in Q1 is a market that is moving forward yet still shaped by structural dependencies and uneven regional dynamics. Demand in Europe remains closely linked to industrial applications rather than the AI driven surges seen in the US and Asia, which makes our progress steadier but also more exposed to external shocks. The challenge now is to maintain this momentum while strengthening resilience across the entire value chain.”

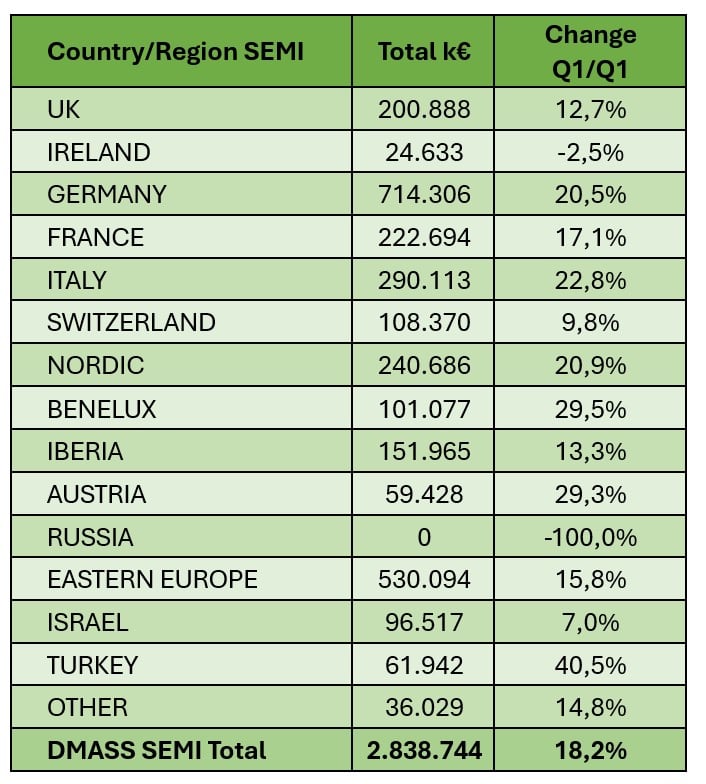

Semiconductors (Q1)

European semiconductor distribution grew strongly to €2.84 billion (+18.2%), driven by a broad industrial recovery but marked by striking regional contrasts. Germany (+20.5%), Italy (+22.8%), the Nordics (+20.9%), Benelux (+29.5%), and Austria (+29.3%) delivered robust double-digit growth, while Ireland (-2.5%) and parts of Southern Europe remained softer.

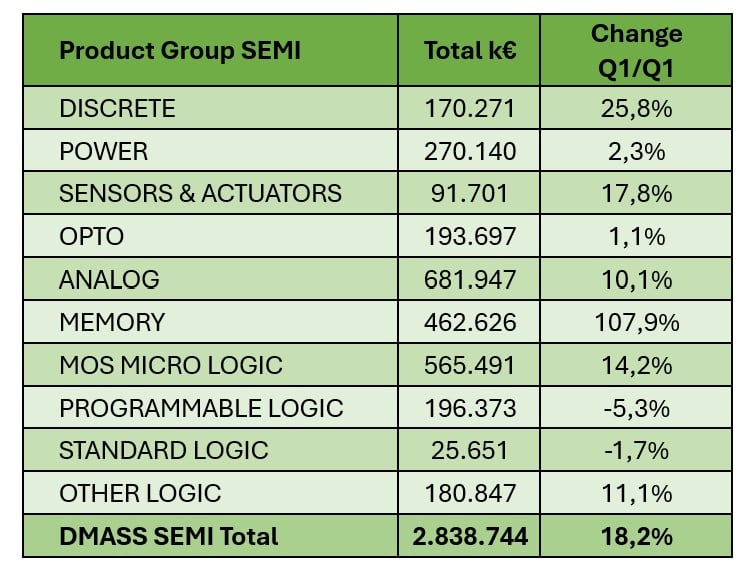

On the product side, the picture is dominated by memory (+107.9%), which has become the single most dynamic segment in the market. Global AI deployments are absorbing enormous volumes of HBM, creating capacity bottlenecks and price increases that are now clearly visible in European distribution. This surge stands in sharp contrast to more traditional segments: discrete devices (+25.8%) and sensors & actuators (+17.8%) continue to grow solidly, while analog (+10.1%) and power (+2.3%) – both closely tied to automotive and industrial applications – show a more measured recovery. At the lower end, programmable logic (-5.3%) and standard logic (-1.7%) remain under pressure from inventory digestion and slower design ins.

Overall, the market is gaining momentum, yet the pattern remains uneven: memory driven growth, structural weaknesses in selected regions, and a European AI cycle that continues to lag the global dynamic. The outlook is positive but rests on fragile foundations shaped by geopolitics, energy price volatility and shifting trade flows.

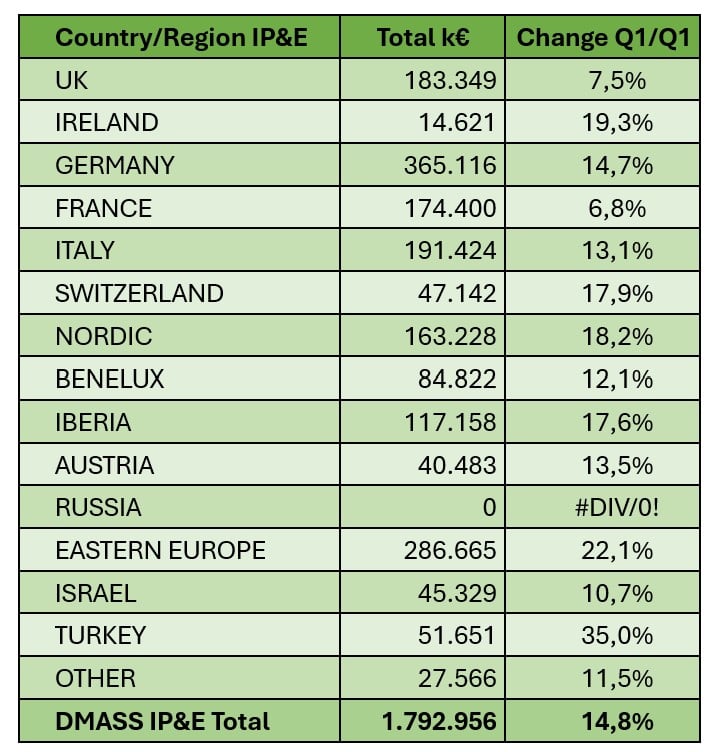

Interconnect, passive and electromechanical components (Q1)

European IP&E distribution reached €1.79 billion (+14.8%) in Q1, reflecting a broad but uneven recovery across the region. Strongest momentum came from Eastern Europe (+22.1%), the Nordics (+18.2%), Ireland (+19.3%), Switzerland (+17.9%), and Iberia (+17.6%), while core markets such as Germany (+14.7%), Italy (+13.1%), and Benelux (+12.1%) delivered solid, steady growth. The UK (+7.5%) and France (+6.8%) expanded more moderately. As in semiconductors, Turkey (+35.0%) stands out with exceptional growth.

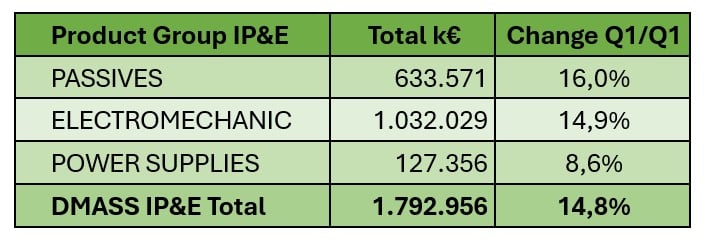

On the product side, the recovery is driven primarily by passives (€633.6 m, +16.0%), which made a strong comeback supported by industrial demand and stabilising lead times. Electromechanical components (€1.03 bn, +14.9%) also performed well, benefiting from automation and infrastructure projects.

Overall, IP&E shows a healthy, broad-based upswing, though with clear differences in regional speed and product specific momentum. The segment continues to reflect Europe’s industrial character: steady, application driven growth with selective pressure points in energy related and power conversion categories.

Reiter concluded: “The first quarter confirms a broad and tangible return to growth across Europe, with both semiconductors and IP&E contributing to a solid upswing. Nearly all major regions posted healthy increases, from Germany, Italy and the Nordics to Benelux and Eastern Europe.

“What stands out most clearly in Q1 is the extraordinary surge in memory, driven by global AI deployments that are absorbing capacity at unprecedented levels. This has already led to tight supply, rising prices, and visible pressure on availability. Europe is more exposed to external shocks because the strongest impulses continue to originate in the United States and Asia. By contrast, traditional industrial segments – from analog and power devices to electromechanical components – show a steadier, more measured recovery, consistent with Europe’s application driven market profile.

The environment remains demanding: supply chain fragility, energy market volatility and the accelerating pull of AI investments outside Europe all shape the competitive landscape. Yet the strengths of European industry remain intact – long term reliability, deep application expertise, and a resilient manufacturing backbone. Q1 demonstrates that Europe is moving forward. The task now is to convert this renewed momentum into sustained progress, greater resilience and a stronger strategic position in a rapidly changing global ecosystem.”