Yole Group announces the release of RF for Defense 2026, its first report dedicated entirely to radio-frequency technologies and devices used in defence applications.

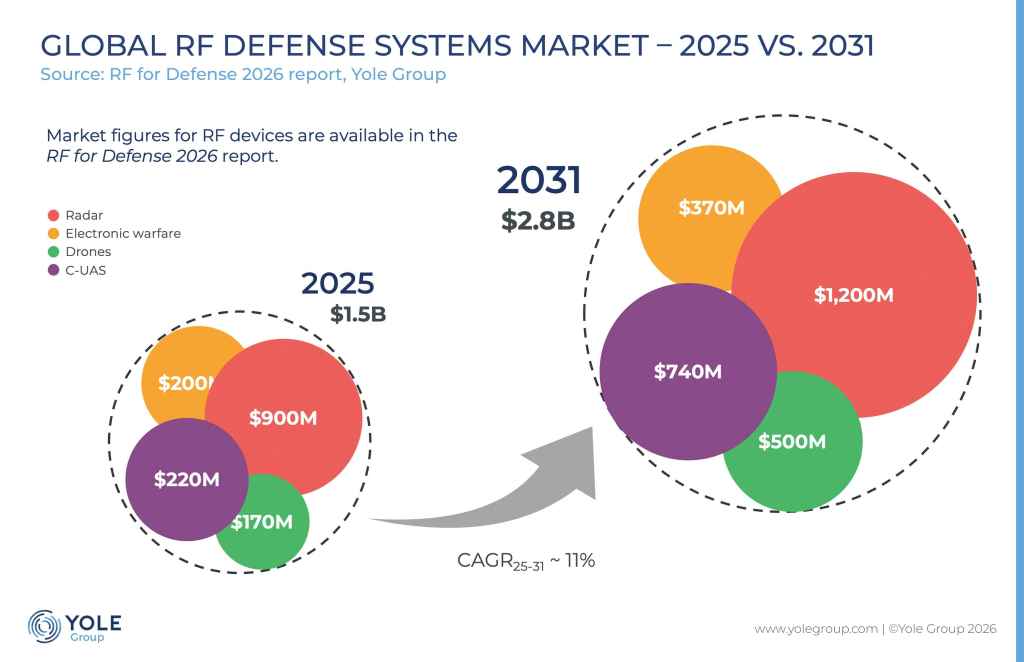

As defence spending increases worldwide and geopolitical tensions continue to reshape procurement priorities, RF technologies are becoming increasingly strategic across radar, EW, drones, and C-UAS. Yole Group’s latest report provides a comprehensive analysis of this evolving market, including forecasts by defence system, RF function, technology, unit sales, and revenue. The study reveals that the RF defence device market is expected to approach $3 billion by 2031, driven by two complementary growth engines: the modernisation of legacy defence platforms and the rapid proliferation of drones and counter-UAS systems.

“The RF defence market is entering a new phase where traditional radar and electronic warfare programs continue to generate strong demand, while drone and counter-UAS deployments are creating entirely new volume opportunities. These two growth engines are reshaping both technology requirements and competitive dynamics across the RF ecosystem,” said Hassan Saleh, Principal Analyst, Radio Frequency at Yole Group.

Today, radar and electronic warfare applications represent the majority of the RF defence device market. Ongoing fleet modernisation programs, replacement of aging systems, and sovereignty driven procurement strategies continue to support demand for high-performance RF technologies, particularly GaAs and GaN devices.

At the same time, the rapid expansion of drone deployments is transforming market dynamics.

Having reached million-unit production scale in 2025, drone systems are expected to increase significantly over the coming years, creating RF requirements that increasingly resemble those found in telecom and consumer markets. Within this segment, C-UAS stands out as one of the fastest growing opportunities, with demand accelerating across portable, vehicle-mounted, and fixed-site systems.

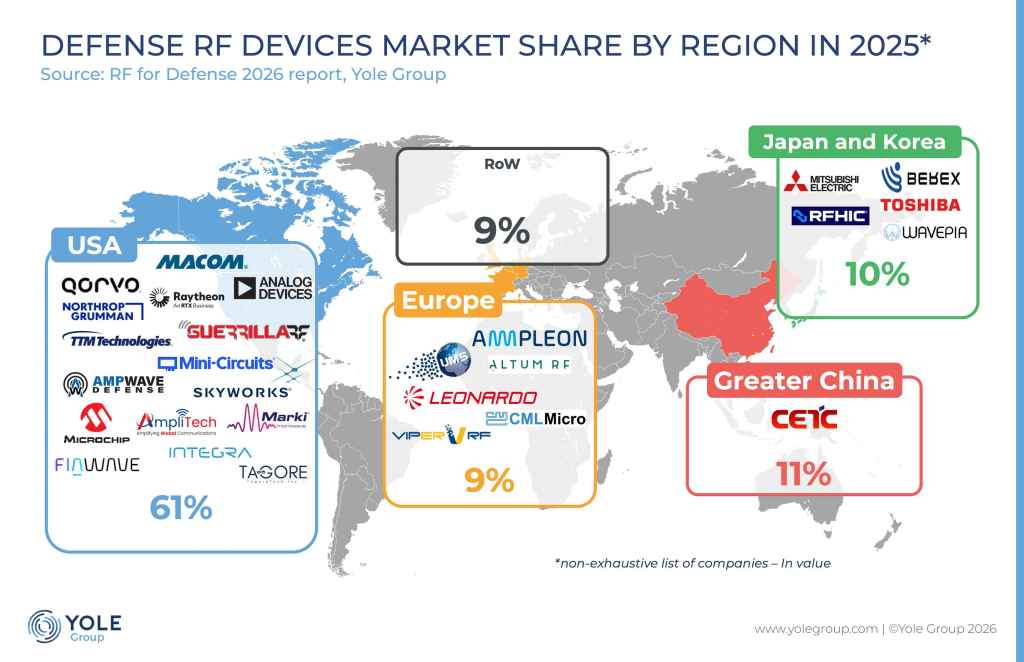

The RF for Defense 2026 report also highlights how the competitive landscape is evolving. While the RF defence system market remains largely structured around sovereign procurement and established defence primes across the United States, Europe, and China, drone and counter-UAS applications are creating opportunities for a broader range of specialised players. New entrants focused on RF detection, jamming, and drone technologies are becoming increasingly important contributors to the defence ecosystem.

Beyond market forecasts, RF for Defense 2026 delivers a detailed analysis of the value chain, competitive positioning, technology adoption, and regional dynamics across the United States, Europe, and China. The report examines the roles of defence system integrators, RF subsystem suppliers, and RF device manufacturers, offering valuable insights into one of the fastest-evolving segments of the semiconductor industry.