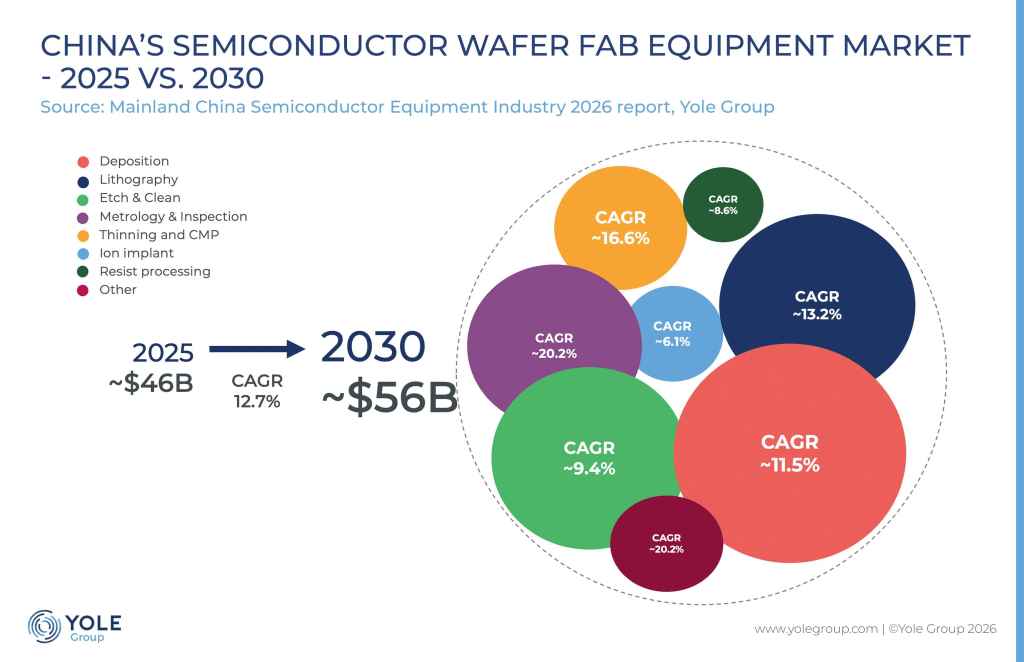

China’s semiconductor equipment ecosystem is entering a pivotal phase. Driven by rising demand for AI computing, increasing memory requirements, and ongoing investments in domestic manufacturing capabilities, the market is moving from ambitious expansion plans to tangible equipment procurement.

A major inflection point emerged in 2026 as China’s leading memory manufacturers accelerated their expansion strategies. CXMT’s planned capacity increase and YMTC’s new fab developments are generating significant demand for key semiconductor manufacturing equipment, including etch, deposition, and chemical mechanical planarization (CMP) systems.

“The synchronised expansion of CXMT and YMTC is not a coincidence. It is an inevitable outcome driven by global demand for AI computing power and supply chain security considerations. Equipment makers will be the biggest beneficiaries of this capacity expansion cycle,” said Merle Zhao, Market Researcher, Semiconductor Equipment, at Yole Group.

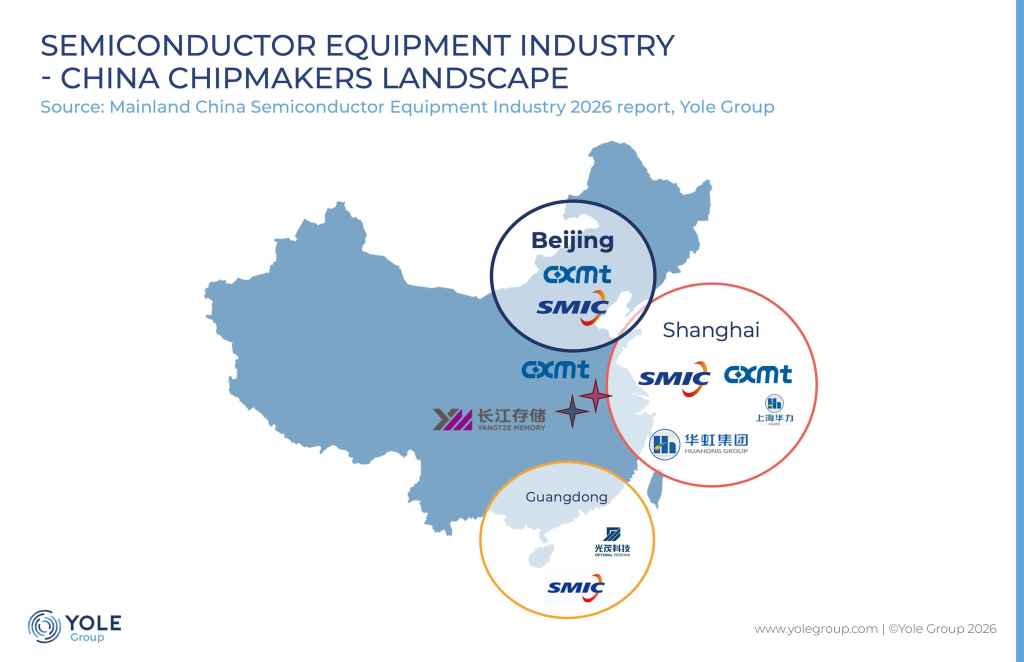

As China concludes its 14th Five-Year Plan, the country’s semiconductor ecosystem continues to strengthen through strategic investments, industrial policy support, and the development of major regional clusters. Beijing, Shanghai, and Shenzhen have emerged as leading hubs for logic devices, while Wuhan and Hefei have established themselves as key centres for memory manufacturing.

The report highlights how China’s strategy to secure semiconductor equipment from domestic suppliers is progressing at different speeds across equipment categories. Etch, deposition, CMP, and thinning equipment have entered a rapid substitution phase, supported by increasing technical maturity and growing adoption by domestic fabs. Other segments, including metrology, inspection, wet cleaning, and ion implant, continue to advance steadily, while lithography remains the industry’s most significant long-term challenge.

Overall, China’s semiconductor equipment localisation rate increased from 8% in 2021 to 23.2% in 2025. According to Yole Group’s analysis, it is expected to reach 39% by 2030, reflecting a transition from policy-driven development toward performance-driven competitiveness.

“A new generation of Chinese equipment suppliers is rapidly gaining ground, transforming the competitive landscape across several key semiconductor manufacturing segments,” said John West, Chief Analyst, Semiconductors Equipment at Yole Group.

For equipment manufacturers, semiconductor companies, investors, and policymakers, understanding the pace and direction of China’s localisation efforts has become increasingly important. Yole Group’s latest report provides a detailed assessment of market opportunities, technology gaps, competitive positioning, and future growth drivers across the semiconductor equipment value chain.