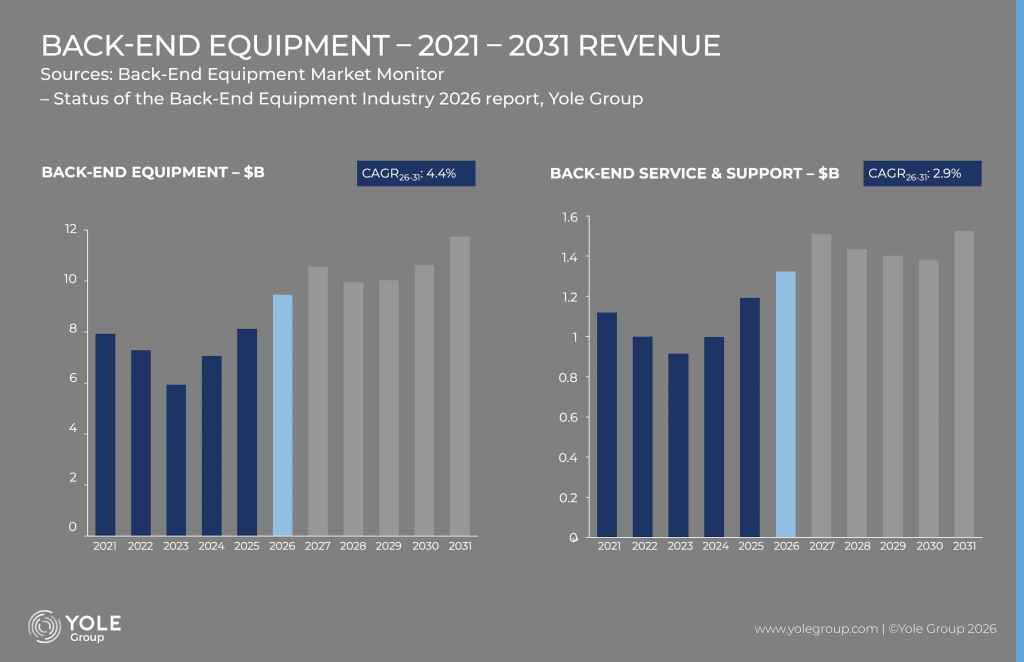

The semiconductor back-end equipment market enters 2026 in a stronger position, though growth is uneven across tool categories. As advanced packaging, HBM, and AI infrastructure capacity come online, customers are prioritising utilisation and yield improvement before launching another major investment cycle. Against this backdrop, Yole Group releases its latest report, Status of the Back-End Equipment Industry 2026, offering a comprehensive analysis of the supply chain, ecosystem, and technology trends shaping the industry’s future.

The strongest demand driver is AI infrastructure, including HBM, high-performance logic, larger package sizes, and tighter logic-memory integration. Unlike a typical semiconductor recovery, spending is concentrated on package complexity rather than tool volume, as customers invest in equipment addressing yield, alignment, warpage, thermal, and interface challenges.

“Advanced packaging is no longer a supporting act. It’s now deciding how fast AI and HBM capacity can scale. And that is reshaping who wins in back-end equipment,” said Vishal Saroha, Technology & Market Analyst, Semiconductor Equipmentat Yole Group.

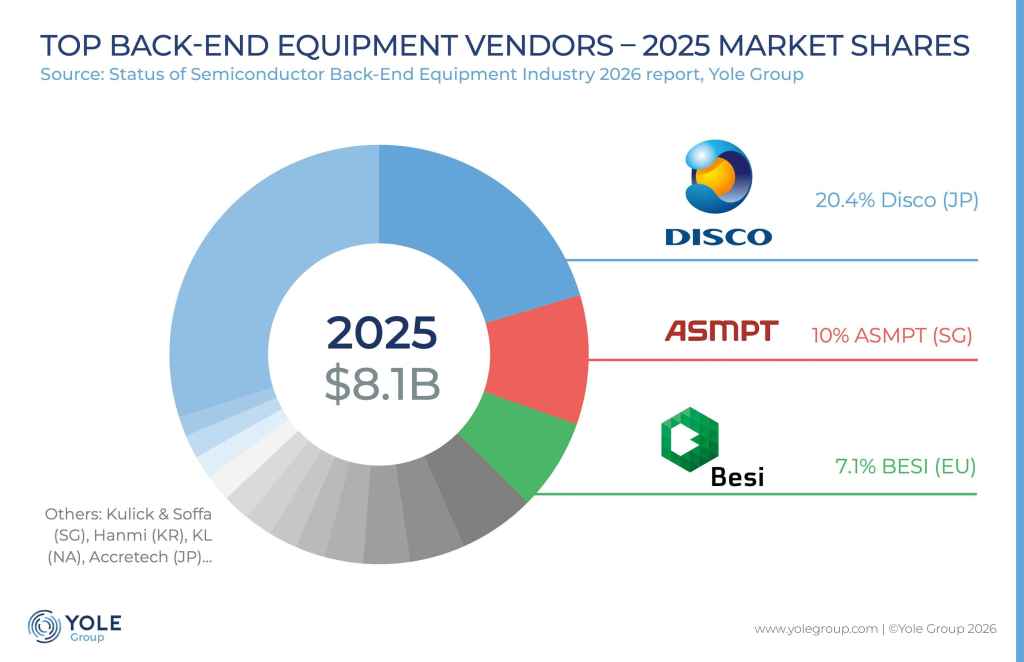

Advanced packaging remains the main supply chain driver. TCB is critical for HBM scaling, with Hanmi and ASMPT as key references, while Hanwha, K&S, and BESI increase their exposure to HBM and advanced logic. Competition in die attach and interconnect is expanding among established, emerging, and Chinese suppliers.

Hybrid bonding now requires coordination across cleaning, metrology, die placement, bonding, and materials: the Applied Materials-BESI collaboration shows adoption depends on a qualified process flow, not a stand-alone tool.

And similar partnerships involving TSMC, Intel, Samsung, SK Hynix, Micron, ASE, Amkor, and JCET reinforce the importance of ecosystem co-development.

Adjacent segments are following suit: DISCO leads dicing as it and peers like Tokyo Seimitsu (Accretech) expand singulation capabilities, while KLA, Camtek, and Onto Innovation benefit from tighter process control requirements.

Regionalisation remains a major trend, with manufacturing and service operations increasingly distributed across China, Southeast Asia, Korea, Japan, India, Mexico, the US, and Europe. Tariffs, export controls, and localisation requirements are pushing suppliers to expand footprints in Malaysia, Singapore, Vietnam, and the US, while US-China tensions encourage OSATs, IDMs, and foundries to diversify. India is accelerating its own ambitions through new OSAT and ATMP projects backed by government incentives.

“The back-end equipment supply chain is being rebuilt around partnerships and resilience, not just capacity. Vendors who secure both will define the next cycle,” said John West, Chief Analyst, Semiconductor Equipmentat Yole Group.

China remains a key part of the landscape: local suppliers are advancing in die attach, bonding, dicing, and hybrid bonding-related technologies, supported by domestic demand. While export controls still limit access to high-end equipment, progress is visible across segments, creating a dual-market dynamic where international suppliers stay essential for leading-edge applications while Chinese vendors close gaps elsewhere.

OSATs, IDMs, foundries, and memory makers all shape different parts of the back-end investment cycle, and equipment suppliers are increasingly engaged earlier in development cycles to hit yield, cost, and scalability targets. By 2031, the back-end equipment leadership will depend on more than tool performance: process integration, installed-base support, regional flexibility, and strategic partnerships will be the key competitive advantages.