The global power electronics industry is entering a new phase. After years of rapid expansion fuelled by electrification and renewable energy, companies are now navigating a more complex environment shaped by overcapacity, pricing pressure, geopolitical tensions, and intensifying competition.

Against this backdrop, Yole Group releases its latest report, Status of the Power Electronics Industry 2026, offering a comprehensive analysis of the market, ecosystem, supply chain, and technology trends shaping the industry’s future.

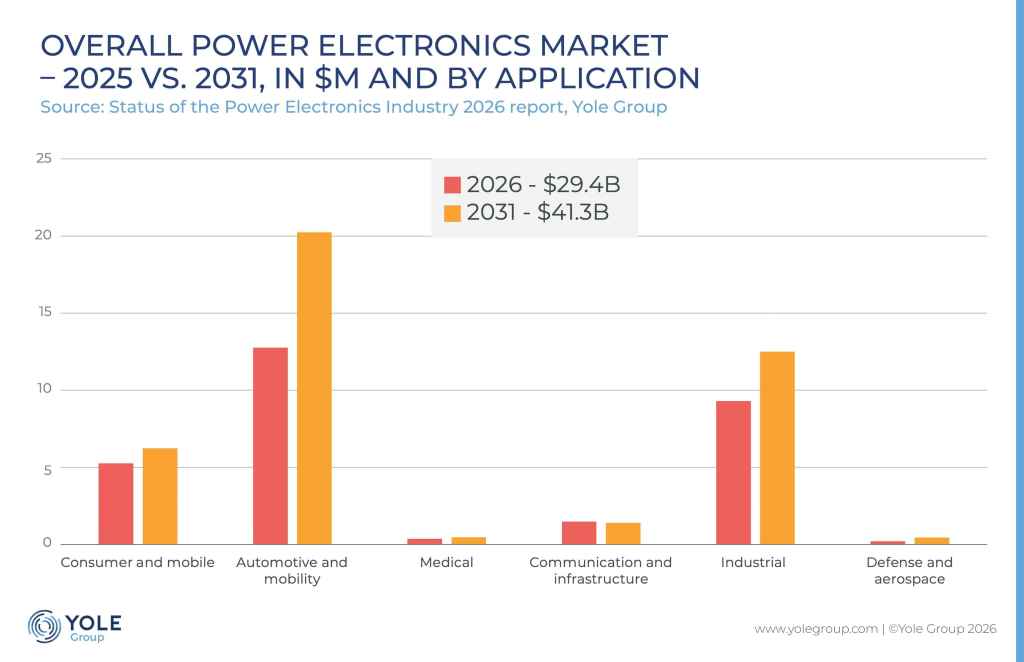

Following a turbulent 2024–2025 period marked by geopolitical uncertainty, lower-than-expected electric vehicle demand, and significant manufacturing overcapacity, the power electronics industry is entering a new phase focused on consolidation, cost optimisation, and competitive positioning. Despite these challenges, Yole Group forecasts the power device market to continue growing at a 7.1% CAGR between 2025 and 2031, reaching $41.3 billion by 2031. While growth prospects remain robust, industry priorities are changing.

“The power electronics industry is entering a new phase: growth continues, but the focus has shifted from expansion to competitiveness, cost optimisation, and market share,” said Milan Rosina, PhD, Principal Technology & Market Analyst, Power Electronics & Battery, at Yole Group.

The 2026 power electronics report provides strategic insight into the forces shaping the future of this industry. They include the rapid expansion of Chinese manufacturers and the evolution of SiC-based solutions and GaN technologies. But there is more. The growing importance of AI infrastructure and data centres, and the increasing role of power electronics in defence and aerospace applications are part of the mix.

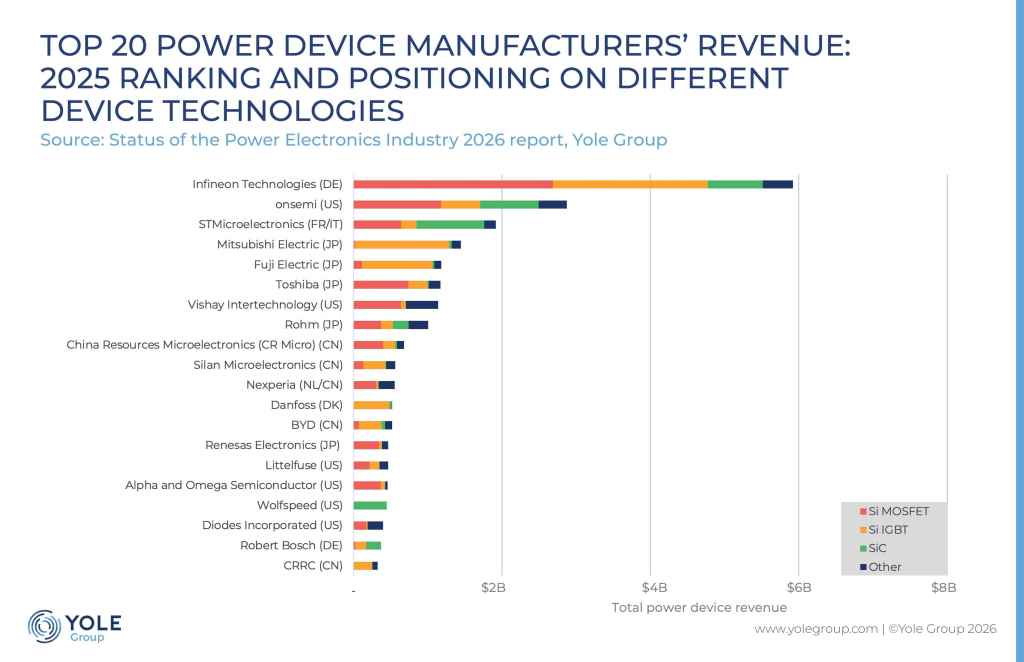

A key feature of this edition is its detailed analysis of the competitive landscape. The report includes updated rankings of the leading power semiconductor companies and examines how investments, mergers and acquisitions, regional industrial policies, and supply-chain strategies are reshaping the market. The report also delivers an updated ranking of the industry’s leading companies. Infineon Technologies maintains its leadership position, followed by STMicroelectronics and onsemi, reflecting their strong capabilities across silicon, SiC, and GaN power semiconductor technologies.

Furthermore, one of the main messages delivered by Yole Group’s analysts is the accelerating rise of Chinese players across the power electronics value chain. Supported by strong domestic demand in electric vehicles, photovoltaics, wind energy, and battery storage systems, Chinese companies are rapidly expanding their presence in SiC wafers, power devices, and industrial power modules, increasing competitive pressure on established global suppliers.

“Power electronics is entering a new chapter. Companies are moving from capacity expansion to profitability, operational excellence, and long-term market positioning,” said Xiran Zuo, Technology & Market Analyst, Power Electronics, at Yole Group.

With electrification, renewable energy deployment, AI-driven infrastructure expansion, and automation continuing to drive demand, understanding the evolution of the power electronics industry has never been more critical for device manufacturers, material suppliers, equipment providers, system integrators, and investors.